Accounting for 20% of the stocks that trade more than 100 thousand units a day in both the HSX and HNX, real estate is one of the most liquid sectors in the stock market. When it comes to price growth, however, the sector was nowhere among the best performers in the market over the past 12 months. While bank, insurance even O&G stocks took turns to join the rally, real estate stocks went mostly sideways during 2015 and the first half of 2016. Even the coming of Circular 06/TT-NHNN, which states that there will be no tightening against mortgage lending until 2017, could not lift enthusiasm for stock property developers more than a couple of days.

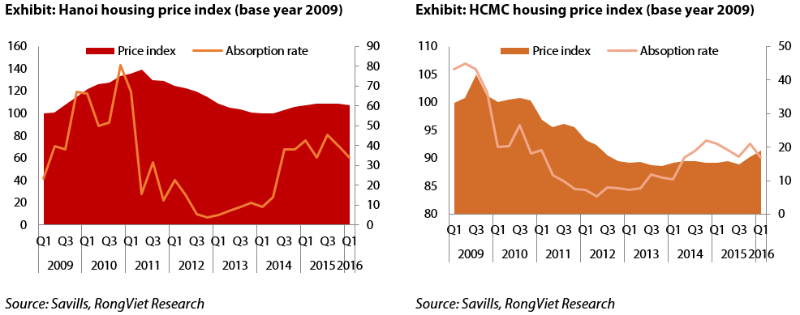

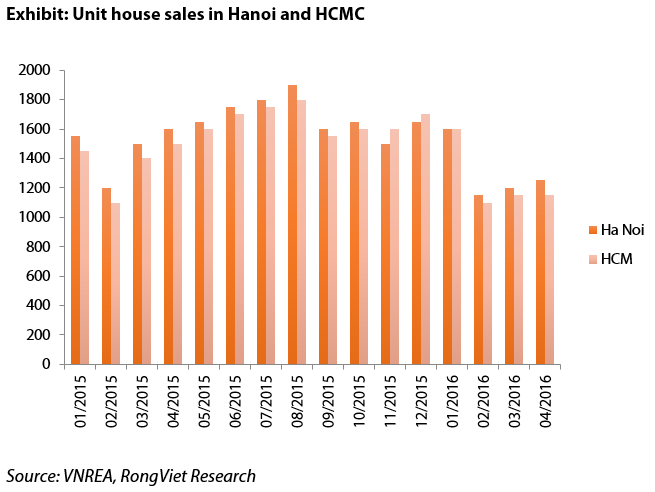

The booming of supply in real estate’s luxury segment when the demand has just recovered is a possible explanation for this. According to Savills, house prices in Hanoi and Ho Chi Minh was largely stable in Q1, yet the absorption rates fell considerably compared to the first quarter and 4Q2015, especially in the middle and high-end segments. The same results can be seen in VNREA’s report, in which Q1 house sales in the two cities decreased sharply from a year earlier. The extent of the drop in absorption rate was somewhat a surprise even though market consensus states that the property market is already past its peak. The abundant supply, the impact of Lunar New Year and the psychological impact of the revision of Circular 36 are the main reasons for this decrease.

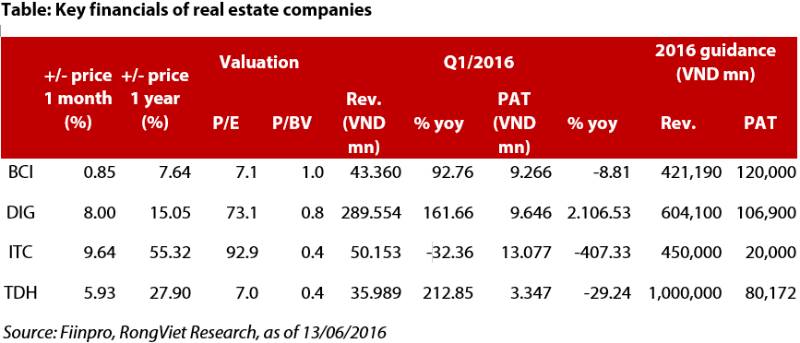

On the other hand, the difference in revenue and profit timing by real estate company is the reason why corporate earnings have not coincided with reported sales. In the first quarter, there are 34/67 listed real estate companies reported positive revenue growth and 35/67 companies reported growth on PAT. Although the result did not show a strong recovery in profitability, abundant liquidity is a favorable condition for the restructuring activities of businesses. Considering this aspect, we highly appreciate some real estatecompanies such as BCI and TDH. Lately, there has also been an increased attention in the market for other companies, such as DIG and ITC.

Regarding of BCI and TDH, two of the most experienced property developers in HCM, expectations for improved business efficiency after restructuring are the main driver for stock prices. In 2016, BCI target a profit-after-tax figure only half that of 2015, which was substantially inflated by non-recurring income. However, we believe that the plan of VND120 billion of 2016 PAT is within reach as it does not take into account the transfer of two land tracts, i.e. 510 King Duong Vuong and 150 An Duong Vuong. There are also high hopes for the cooperation between BCI and KDH following KDH’s acquisition of 57% BCI’s chartered capital. Nonetheless, we believe the synergies would only begin to realize after 2017, by which time KDH has finished its remaining projects in District 2 and District 9 and BCI has completed the necessary legal works and infrastructures for its major projects such as Corona City, Phong Phu 2, Tan Tao Urban Area…

Unlike BCI, TDH commits to achieve 70% year-over-year growth in its profit after tax in 2016 given the strong ability to recognize the sales of 168 apartments from TDH - Phuoc Long along with several finished projects such as Phuoc Long Spring Town, Long Hoi City… Most of TDH’s projects have high compensation rates and ready LURs. In addition, recent handshakes with Fideco and Lien Phuong Textile are expected to create the firm foundation for TDH’s long term growth. Of the most recently acquired projects, the project at 28 Phung Khac Khoan (co-developed with Fideco) and the project at 39 – 41 – 43 Vo Van Kiet (co-developed with Lien Phuong Textile) are considered the most potential thanks to their very prime locations.

BCI, TDH, DIG and ITC are all ex-SOE real estate businesses who were able to accumulate a large, low-cost land bank. DIG announced in the last week of May that it would liquidate a number of its projects including such as Dai Phuoc Eco Urban Area - Dong Nai (13.43ha), Nam Vinh Yen - Vinh Phuc New Urban Area (2 plots of 9,300m2 in total), Chi Linh - Vung Tau City Center (2 plots of 1.45ha in total) and An Son Hill Villas - Da Lat. Though estimated profits from these transactions are not that promising due to capitalized interest expenses, the move is expected to enable DIG to recover the initial investments and free up cash for betterprojects. In 2014, ITC also withdrew from Intresco Tower at a substantial loss but retrieved capital to trim its debts by a half. Beside Long Thoi- Nhon Duc Residential Area (55ha in Nha Be), ITC also invests in a prominent project at No. 83 Ly Chinh Thang, Q3, HCMC. Due to clearance problems, the company has not managed to boost the progress. Successfully resolving the problem can be an important step for ITC to get back to the growth path.

With their experience and large land bank, BCI, TDH, ITC and DIG each can become a big player by its own virtue. TDH, DIG and ITC are trading at a low price compared to their BV. Before being acquired by KDH, BCI were trading at a P/B around 0.6x. It can be inferred from this that, given their existing advantages, a catalyst, either it is a new owner or a liquidation of a major project is all these companies need to reignite their growth engine.

Rongviet Research