AFC chính thức chạy quỹ vào tháng 12 năm 2013, với số vốn ban đầu chỉ 3.6 triệu đô, đến nay đã lên 10 triệu đô, AFC chuyên đầu tư vào những doanh nghiệp vừa và nhỏ tại Việt Nam, và xem đây là lợi thế của riêng mình vì những đối thủ lớn hiện tại hầu hết vẫn chọn những doanh nghiệp lớn. Ngoài ra, định giá cổ phiếu của nhóm cổ phiếu nhỏ đang khá rẻ, chỉ là 7x vào tháng 12 năm 2013, trong khi đó chỉ số này của toàn thị trường lên đến 11x vào thời điểm đó.

Trả lời câu hỏi tại sao chọn Việt Nam, AFC trả lời thị trường chứng khoán Việt Nam đã điều chỉnh rất mạnh kể từ đỉnh năm 2007, và đây là cơ hội hiếm hoi để mua hàng giá rẻ. Ngoài ra, Việt Nam có dân số trẻ, đông và có trình độ học vấn khá tốt.

Trả lời câu hỏi và xử lý nợ xấu, AFC đồng quan điểm với Andy Hồ, quá trình xử lý nợ xấu của Việt Nam diễn ra khá chậm, nhưng tin tưởng vào khả năng những khoản nợ xấu này trở nên hết xấu nhờ bất động sản tăng giá và quy mô GDP tăng trong thời gian tới.

Trả lời câu hỏi về việc lần đầu tiên Việt Nam áp thuế chống bán phá giá đối với lĩnh vực thép để bảo hộ hàng nội địa, AFC cho rằng đây là việc rất cần thiết và nên làm.

Xem bản chi tiết bên dưới.

-----------------------------------

Kinh tế VN trong mặt quỹ ngoại AFC, cập nhật 10/12/2013

Một Quỹ nước ngoài mới thành lập đầu tư chủ yếu vào Việt Nam có những nhìn nhận cập nhật về Việt Nam như sau:

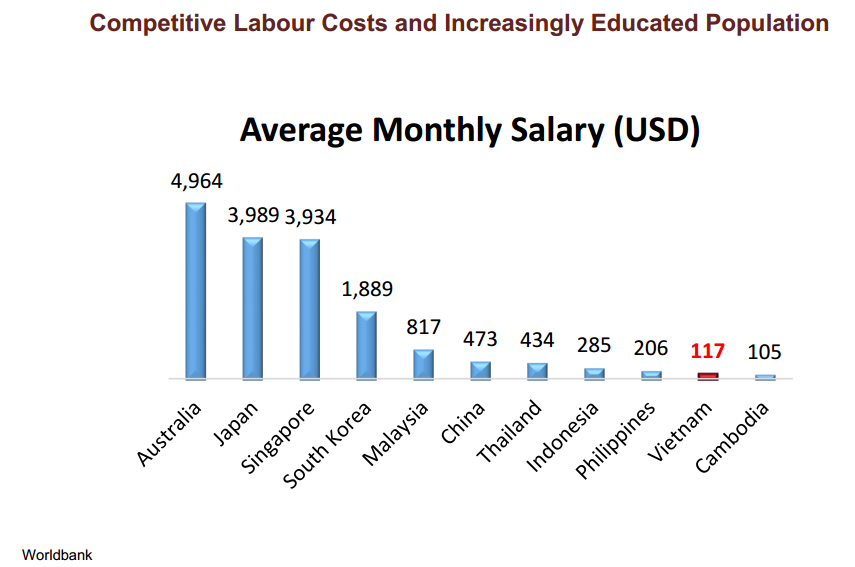

1. Chi phí lao động rẻ và số người học vấn tăng:

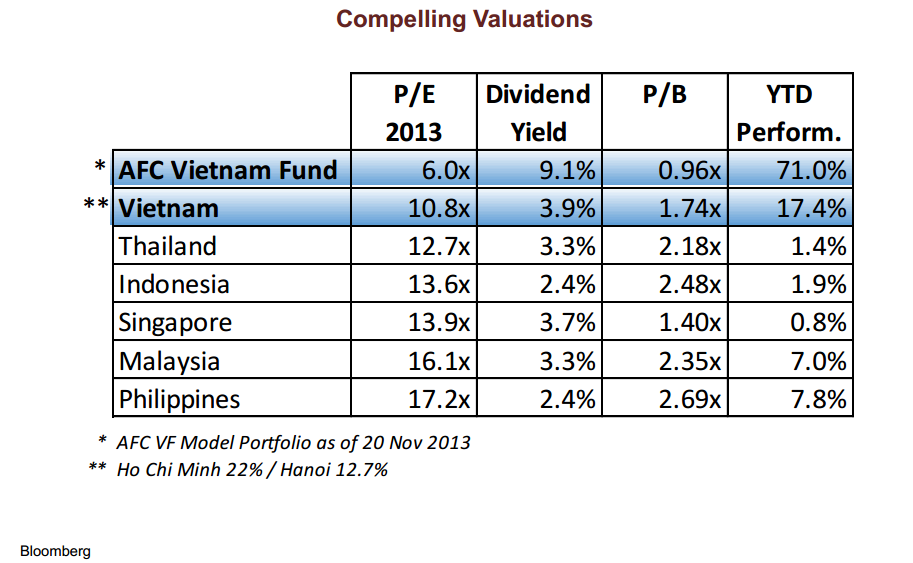

2. Định giá hấp dẫn:

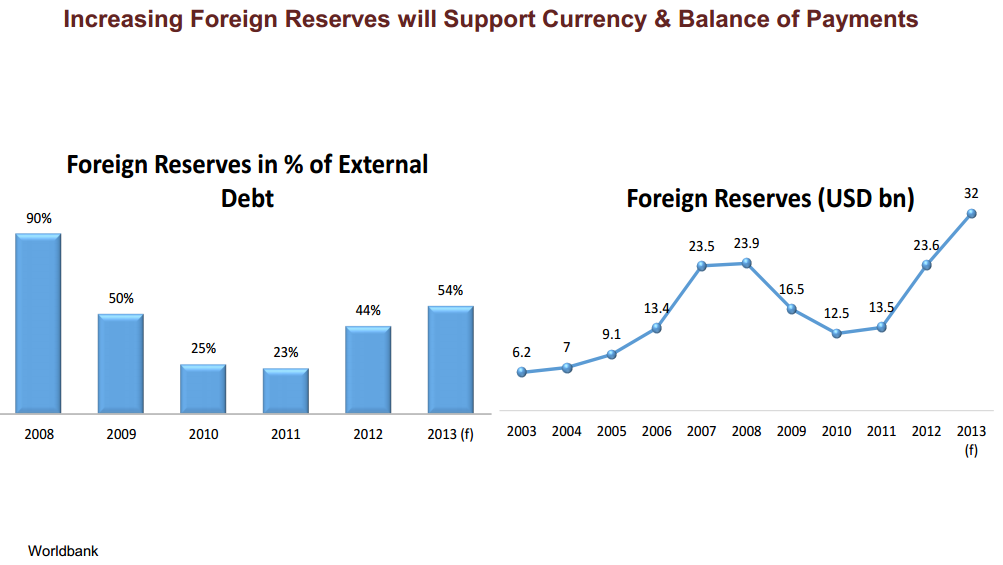

3. Dự trữ ngoại hối tăng mạnh:

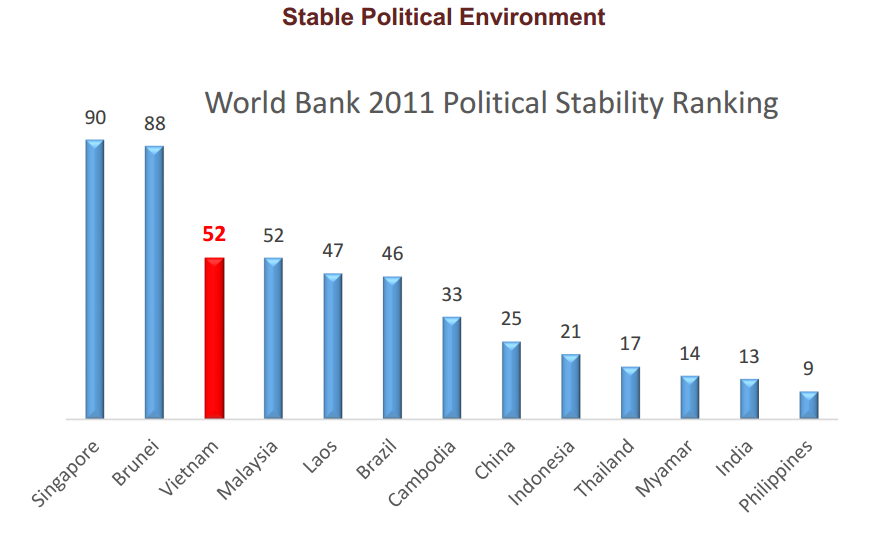

4. Môi trường chính trị ổn định:

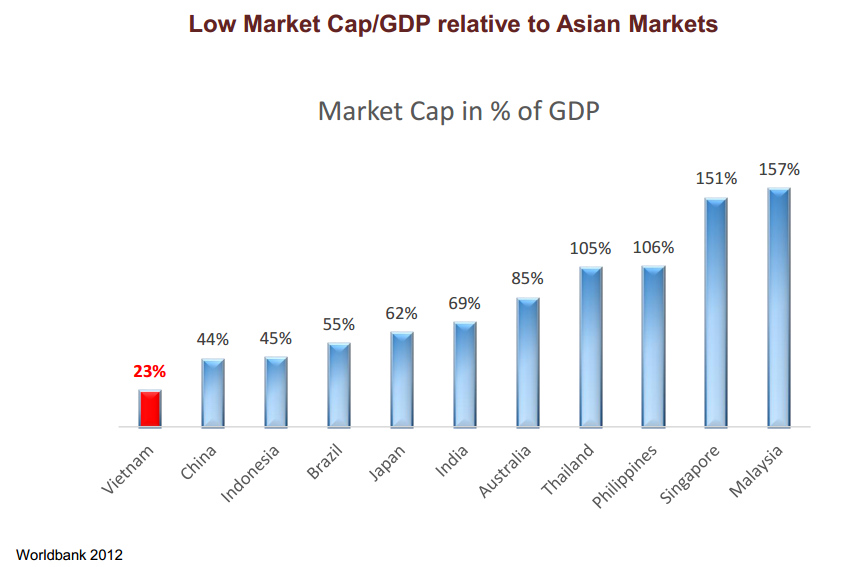

5. Vốn hóa thị trường trên GDP thấp so với các nước trong khu vực:

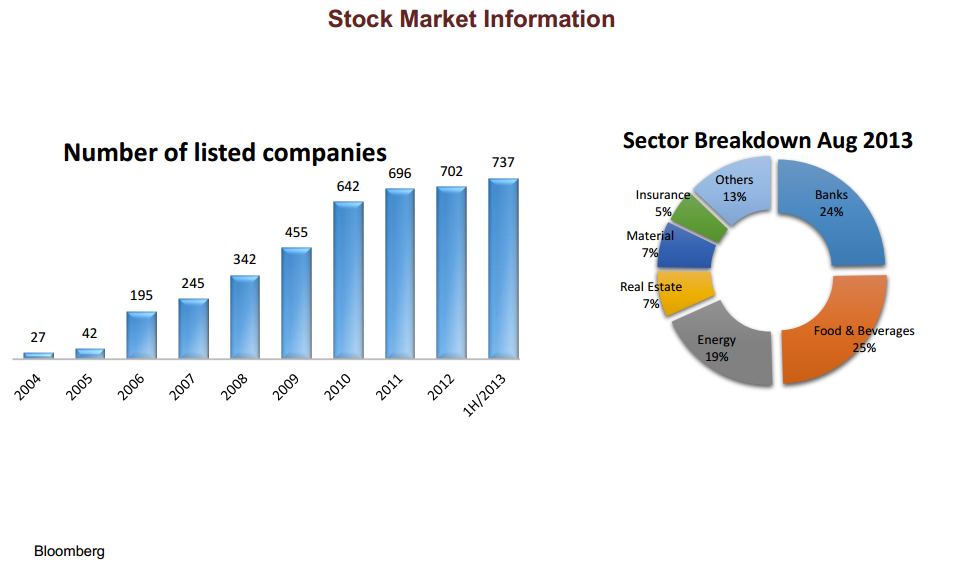

6. Hàng hóa trên thị trường chứng khoán dồi dào hơn:

Nguồn: finandlife|AFC

--------------------------------

Andreas Vogelsanger, CEO of Asia Frontier Capital Vietnam (AFC Vietnam), is bullish on Vietnam. The parent company to his fund, Asia Frontier Capital, is a public equity investment outfit that invests in emerging and frontier public equity markets across Asia in its Asia Frontier Fund. Mr. Vogelsanger works closely with Asia Frontier Capital CEO Thomas Hugger who formerly ran the public equities arm of Leopard Capital before buying out that portion of the business and rebranding it as Asia Frontier Capital.

Mr. Vogelsanger came to AFC Vietnam with 25 years of experience in the finance industry with stops at EVK Capital Singapore, Coutts Private Bank in Hong Kong and Singapore, and Bank Julius Baer in both Zurich and Singapore. AFC Vietnam launched in December 2013 as the first single country fund of Asia Frontier Capital, and the firm’s second fund. AFC Vietnam Fund distinguishes itself from many peer Vietnam funds by offering investors the opportunity to invest in the small-cap and mid-cap sector of Vietnam’s capital markets. In this interview Mr. Vogelsanger sheds some light on how Vietnam’s stock markets are doing beyond the large caps that dominate the indices.

Jon Springer: How is your fund performing compared to Vietnam’s stock exchange index which is up about 24% year-to-date?

Andreas Vogelsanger: Asia Frontier Capital Vietnam Fund launched in December 2013, just before the start of this year, and is up 27% since launch. We started small with USD 3.6 million in assets under management and are now at almost USD 10 million. We use our small size to our advantage to be more nimble in the market.

Springer: The largest investment funds to invest in Vietnam’s public equity markets are run by Dragon Capital and VinaCapital. How does your fund offer a different opportunity to engage the market?

Vogelsanger: We focus on small and mid-cap companies in Vietnam. Keep in mind, what is small-cap in Vietnam would probably be micro-cap by European standards. Funds like VinaCapital & Dragon don’t have the same flexibility because they have funds so large they cannot meaningfully invest their portfolios in companies as small as the ones we predominantly do.

Part of the issue investing in Vietnam is waiting for a revaluation of the market. When we started in December 2013, the price to earnings ratio for the whole market was around 11. Now, the market is more in-line with peers around Asia with a price to earnings ratio around 14. However, our small to mid-cap segment is still around 7 where we started off in December 2013. There hasn’t been a repricing in our sector to benefit from yet, though we think it will come. As our methodology has chosen investments well, our fund has kept up with the market even though our investment category’s price to earnings ratios have not.

At a later date, when the small to mid-cap stocks in Vietnam become more expensive, we may change strategies to meet the best opportunities the market presents.

Springer: Vietnam has experienced rapid growth and bubbles popping in the last decade. Has the government learned how to manage the economy better from the bubbles popping?

Vogelsanger: In my perception, yes. When I spoke to local people in 2013 before launching the fund, business people were not that positive. Despite this, our chief investment officer Andy Karall and myself thought that a lot of things were pointing toward a sustainable recovery.

Critics often say the government is not doing things fast enough, but this is often the case in many countries. They are tackling all the right issues and these things take time. By no means is everything perfect – but they do have sound monetary policy, currency stability, inflation under control, interest rates going lower, bank issues being addressed and FDI increasing – these are all signs of stability that should give confidence to investors.

Springer: Why did Asia Frontier Capital choose Vietnam as the first country for a single country focused fund?

Vogelsanger: The correction between 2007-2012 was almost 90% on the Ho Chi Minh stock exchange and 70% on the Hanoi stock exchange top to bottom. Corrections like these create opportunities. The Asia Frontier Fund itself has roughly 20% of holdings invested in Vietnam because of our conviction that Vietnam is a good investment.

Vietnam has a lot of other factor going for it including a population that is very well-educated compared to peer nations as noted by the OECD’s Program for International Student Assessment report, as well as a young population that works hard for low wages. [The PISA report compares education in 65 countries around the world. For methodology, you can watch this video; Vietnam's surprisingly good results - just behind Germany and well ahead of the United States - are on the below chart.]

Vietnam ranks just behind Germany in education according to 2012 results. The next tests will be in 2015. (Source: Asia Frontier Capital Vietnam; PISA; OECD)

We started investing in 2013 prior to launch with a qualitative approach built by our CIO Andy Karall that he had used in the past to see how it would work in Vietnam’s market. We successfully calibrated our model to the Vietnamese stock market and managed to significantly outperform the overall market – even much better than this year’s outperformance – so we proceeded to raise capital and launched the fund.

Another factor that benefits our focus on small to mid-cap companies is that we have very few competitors in this space. Whereas investment funds investing in large-cap companies may run into Vietnam’s limits on foreign ownership of stocks, the companies we invest in are under-invested by foreigners so we never have to concern ourselves with the foreign ownership law.

Springer: Vietnam has recently announced anti-dumping tariffs on stainless steel imports from China, Taiwan, Indonesia and Malaysia. What does this do for Vietnam’s steel producers and what does it say about government policy toward local business?

Vogelsanger: This is the first time that the government is trying to impose these type of anti-dumping tariffs. Tarriffs are now between 3% and 39% depending on the type of steel. To my knowledge, this is the first time the government is taking such strong measures to protect the domestic market. Local producers went through a lot of pain to modernize their production lines so they would have the capacity to cover domestic demand but they cannot compete with prices from other countries.

There is a question of if these tarriffs will trigger a chain of reactions. From a trading partner point of view, Taiwan and China are more important trade partners than the other countries. A trade war with these countries would not be advisable or beneficial but so far stock markets have not reacted to the news.

Springer: When it comes to Vietnam, the common point of view is that the major risk to Vietnam’s ongoing recovery is cleaning up the banking sector and its non-performing loans (NPLs). How is this progressing?

Vogelsanger: Vietnam Asset Management Company [a government agency] has been addressing the right issues of dealing with NPLs and banking regulations, but it has not yet taken on the pace one would have hoped for in terms of speed. They have been selling off the NPLs, but its not rapid enough. Andy Ho of VinaCapital [CIO of VinaCapital Vietnam Opportunity Fund and other funds] recently said in an article, “NPLs are hard to solve but Vietnam can inflate its way out of this.”

Personally, I think the problems may solve themselves if growth returns and the real estate market picks up. GDP growth at the top end is expected at best to be 6% this year. Vietnam probably needs more growth than that to clean things up, though this is just a back of the napkin estimate.

To be the next China, as I think Vietnam can be, they will need to accelerate growth to around 9%. Interestingly, Intel has said it took 14 years in China to adapt the workforce to their methods, but only took 4 years in Vietnam. Fact-based public relations like this is a big positive for Vietnam’s future growth.

* Author’s note for the purposes of comparison: Dragon Fund’s two largest funds, VEIL and VGF, were up 21.86% and 17.93% year-to-date respectively as of a September 11, 2014, update from the firm; VinaCapital’s flagship Vietnam Opportunity Fund was up 20.35% year-to-date as of September 26, 2014. All three funds are closed-end funds that currently trade at a discount which in all cases has moderated this year.

Nguồn: finandlife|http://www.forbes.com/