Ngân hàng Trung ương châu Âu (ECB) vừa tuyên bố sẽ bơm ít nhất 1.1 ngàn tỷ EUR (tương đương 1.3 ngàn tỷ USD) vào nền kinh tế Eurozone. Theo đó, hàng tháng ECB sẽ mua 60 tỷ EUR (70 tỷ USD) trái phiếu cho đến hết tháng 9/2016. Đây là động thái nhằm chống lại đà suy thoái chưa có dấu hiệu bị đẩy lùi, giảm phát bắt đầu quay trở lại những tháng gần đây.

Kể từ tháng 10 năm 2014, Euro đã bắt đầu thực hiện các biện pháp nới lỏng tiền tệ nhằm cứu nền kinh tế Lục Địa Già, theo đó, ECB giảm 3 loại lãi suất chủ chốt xuống mức thấp kỷ lục và mua các chứng khoán bảo đảm bằng tài sản (ABS), trái phiếu đảm bảo. Việc chính thức thực hiện QE như tiên bố gần đây là một liều thuốc mạnh hơn để giúp nền kinh tế không rơi vào vòng xoáy suy thoái.

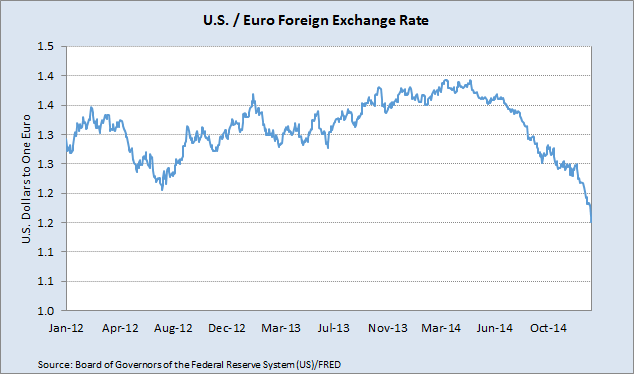

Trong lúc ECB tích cực bơm tiền ra thì FED lại thực hiện taper QE và tuyên bố nền kinh tế đã hoàn toàn qua giai đoạn khủng hoảng, điều đó đã làm cho đồng Euro suy giảm và đồng USD tăng giá, tương quan của 2 đồng tiền này được thể hiện như hình bên dưới, theo đó, đồng Euro sẽ còn tiếp tục suy giảm trong thời gian tới.

---------------------

There are six key elements to the ECB’s announcement:

1. Starting in March the ECB will buy 60 bln euros a month in national bonds and agency bonds. The amounts will be driven by the “capital key” which corresponds roughly to the size of the economies. That means that Germany, France and Italy will be the largest buyers.

2. The risk will remain largely with the national central banks, but the risk of agency purchases will be shared collectively. Agency bonds will amount to 12% of the assets being purchased. The ECB argues that by controlling all the design features and coordinating the purchases, it has “safeguarded the singleness of the Eurosystems’s monetary policy. “ Market participants may disagree.

3. The program will run through September 2016, but ECB clearly keeps door open: the purchases “will in any case be conducted until we see a sustained adjustment in the path of inflation.”

4. The asset purchased will be investment grade, but “some additional eligibility criteria will be applied in the case of countries under an EU/IMF adjustment program." This is subtle but important. As long as Greece, Cyprus and Portugal are on some program their bonds can be bought. This is also a subtle indication that the old Troika no longer exists. This is part of the signal from the European Court of Justice preliminary ruling, and also the signals from the new EC.

5. Although the ECB did not cut its official rates, it did remove the 10 bp premium over the main repo rate (MRO) for the new TLTRO facility.

6. There is an issuer limit of 33%. This is why Draghi has indicated that Greek bonds could be bought after SMP redemption, which means after July.

Source: finandlife|http://www.marctomarket.com/