SINGAPORE—Adventurous investors looking for big returns are pouring billions of dollars into frontier markets, but big fund managers say recent gains are too much, too soon.

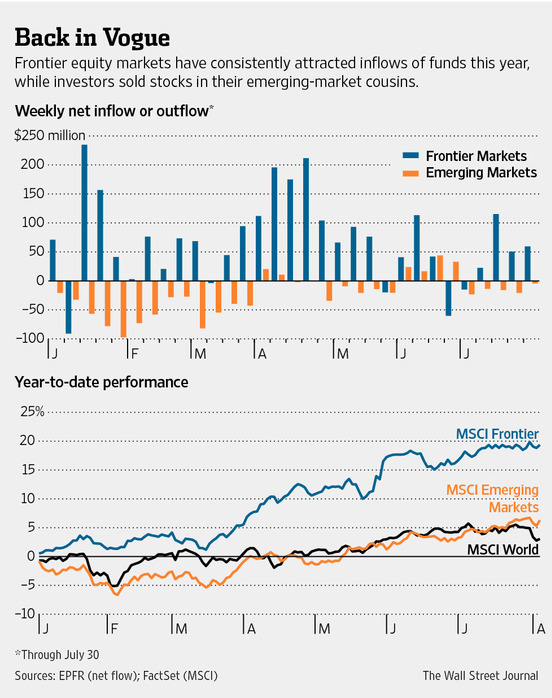

Foreign funds have pumped $2.2 billion this year into the world’s frontier markets, which range from Argentina to Vietnam and rank as the smaller, lesser-known cousins of emerging markets. That compares with a net $720 million withdrawal from emerging markets, according to data from EPFR, a fund tracker.

The result is that as of Tuesday, the MSCI Frontier Markets Index had risen 19% year to date, compared with gains of just 6% in the MSCI Emerging Markets index and 2.2% in the MSCI World benchmark. That makes frontier markets some of the world’s best performers, but is also drawing concern that it is the tide of cash flowing into these small markets, rather than improving investment prospects, that is driving the gains.

The rally and pouring in of money have been virtually uninterrupted, even as markets in the U.S., Europe and some parts of the emerging world have started to wobble in recent weeks.

“There is an almost desperate attempt on the part of investors to capture the gains people have seen in emerging markets over the last decade [and] a real desire to believe that you can get returns in the low to mid-teens,” said Kemal Ahmed, a portfolio manager and head of Investec Asset Management’s frontier investments. Investec manages $123 billion globally.

The attraction to these fast-growing markets has been widespread. In June, Norway’s $886 billion sovereign-wealth fund, the largest in the world, jumped on the bandwagon to add frontier markets to its investments.

The problem for many investors is the opportunities in frontier markets are few and competition is fierce. Foreign ownership of many companies in the index has already reached government limits.

Ten stocks account for more than 35% of the MSCI Frontier index, according to MSCI data, and companies in Kuwait comprise nearly a quarter of the overall index’s market capitalization. Nigeria accounts for a fifth.

The total market capitalization of all stocks included in the MSCI Frontier Markets index is $109 billion, according to MSCI, compared with $4 trillion in the equivalent emerging-market index. Given the markets’ size, some investors worry about a potential, sudden race for the exits. With thin liquidity, executing sales quickly could drive frontier markets sharply lower, if buyers could be found at all, they say.

Fund managers say part of the reason frontier markets appear to have performed so well this year that some countries have been reclassified. Qatar and the United Arab Emirates were considered strong enough to be upgraded to emerging status in June, shrinking the realm of frontier markets and concentrating the flow of foreign cash into fewer countries.

Gains in the remaining frontier markets have been amplified. In the year to date through Wednesday, Vietnam’s Hochiminh VN Index has risen 20% and Pakistan’s KSE 100 is 16% higher, while Argentina’s Merval index was 50% higher as of Tuesday. In the first six months of the year, frontier-market investors tracked by Morningstar Inc. MORN -1.06% earned an average return of 9.8%, compared with 4.7% in developed markets.

Some funds have been able to claim extraordinary gains in the first six months of 2014, according to the Morningstar data. Several frontier funds managed by Schroders SDR.LN -0.99% PLC, for example, have achieved percentage returns in the high teens.

Thomas Vester, global chief investment officer at LGM Investments, which is part of BMO Global Asset Management, says frontier investing can still provide opportunities to those who can negotiate the political and corporate- governance problems that these fledgling markets present. Valuations in frontier markets don’t seem excessively high yet, with dividend yields of about 4%, compared with 2.5% in emerging markets. Mr. Vester says.

LGM has $881 million invested in frontier-market funds. Mr. Vester is particularly keen on Vietnam, Bangladesh and Pakistan.

Still, he warns that as a result of the hunt for high returns, money is being pumped into “less prudent companies.” Funds are flowing into frontier fixed-income investments, as well as equities, he notes.

Ecuador, for example, sold $2 billion worth of junk-rated 10-year bonds in June, just eight years after a default in 2008 on $3.2 billion of debt. The sale followed an issue of the same size by Kenya a day earlier, which attracted $8 billion of orders.

Other investors are more cautious. “The creation of massive liquidity in the U.S., Europe and Japan, created by quantitative easing and zero-interest rate policies, has lowered the bar for investor returns and it takes very small capital flows to push these markets up,” says Peter Marber, a fund manager at Loomis Sayles & Co. in the U.S., which manages about $221 billion.

Mr. Marber manages investments in both frontier and emerging markets and says he prefers larger emerging markets this year because their relatively poor performance compared with other asset classes have made valuations attractive.

Investors must remember that frontier markets are highly volatile and risky, warns Mr. Marber. “Frontier markets are the ultimate caveat emptor,” he says.

http://blogs.wsj.com/