by finandlife08/01/2024 09:11Theo báo chí trong nước, CTG công bố kết quả sơ bộ với những thông tin chính như sau:

- Tăng trưởng tín dụng năm 2023 là 15% so với mức tăng trưởng tín dụng 9 tháng đầu năm 2023 là 8,7%, so với dự báo cả năm của chúng tôi là ~13%

- Tăng trưởng huy động năm 2023E là 13,7% trong đó số dư CASA tăng 27%, hàm ý tỷ lệ CASA có thể rơi vào khoảng 22% so với dự báo cả năm của chúng tôi là 20,5%

- Tỷ lệ nợ xấu năm 2023E là 1,15% so với dự báo cả năm của chúng tôi là 1,40% với tỷ lệ bao phủ nợ (LLR) là 160% so với dự báo cả năm của chúng tôi là 170%

- LNTT 2023 không được công bố; tuy nhiên, ban lãnh đạo đã thông báo rằng ngân hàng đã hoàn thành mục tiêu về lợi nhuận của mình. CTG đặt mục tiêu LNTT riêng lẻ năm 2023 là 22,5 nghìn tỷ đồng (+10,6% YoY), ngụ ý LNTT hợp nhất năm 2023 là khoảng 23,3 nghìn tỷ đồng (+11,4% YoY,) so với dự báo LNTT hợp nhất cả năm của chúng tôi là 22,9 nghìn tỷ đồng (+9,2% YoY)

Nhìn chung, kết quả năm 2023 có vẻ tốt hơn chúng tôi dự đoán nhờ tỷ lệ nợ xấu thấp hơn dự kiến. Chúng tôi chờ báo cáo tài chính năm 2023 để có thêm thông tin về chi phí tín dụng và tỷ lệ xử lý nợ để đánh giá cụ thể hơn bức tranh lợi nhuận của ngân hàng.

VIETCAP RESEARCH

====

2ebc3fa3-1eea-404e-87c3-0fecdf6741f7|0|.0|27604f05-86ad-47ef-9e05-950bb762570c

Tags: CTG

Stocks

by finandlife03/01/2024 08:52

Nguyen Duc Hung Linh

2 years ago, suggesting VietQR for money transfers was met with blank stares. Today, it's everywhere, from shopping malls to wet markets. The rapid popularity of VietQR is phenomenal, especially when compared to the hefty marketing budgets burned by fintech companies. 🤔 Why has VietQR become so popular so quickly?

1 Merchants prefer VietQR for its zero fees and instant money reception. In June 2021, NAPAS launched VietQR alongside NAPAS 247, a service enabling instant, real-time, and zero-fee money transfers between bank accounts. NAPAS 247 disrupts fee-based QR payment services offered by E-wallets or payment gateway companies like VNPay and MOMO.

2 Commercial banks also find VietQR beneficial; more merchant use means more Current Account and Savings Account (CASA) for banks 💰. Banks distribute printed QR codes for merchants, turning hundreds of thousands of bank employees into inadvertent VietQR promoters.

3 End consumers might feel indifferent initially, but more are leaning towards VietQR. Peer-to-peer money transfers through bank apps' QR code generation and scanning make transactions easier. People tend to stick to what they use more often.

What's the impact on the payment landscape?

1 As VietQR gains traction, the usage of VNPay or MOMO diminishes. Fintech giants are compelled to explore alternative strategies for customer retention and revenue generation. VNPay leverages unique features within commercial banks' apps, while other e-wallets strive to evolve into super apps. The path to profitability for these fintech companies has undoubtedly become more challenging.

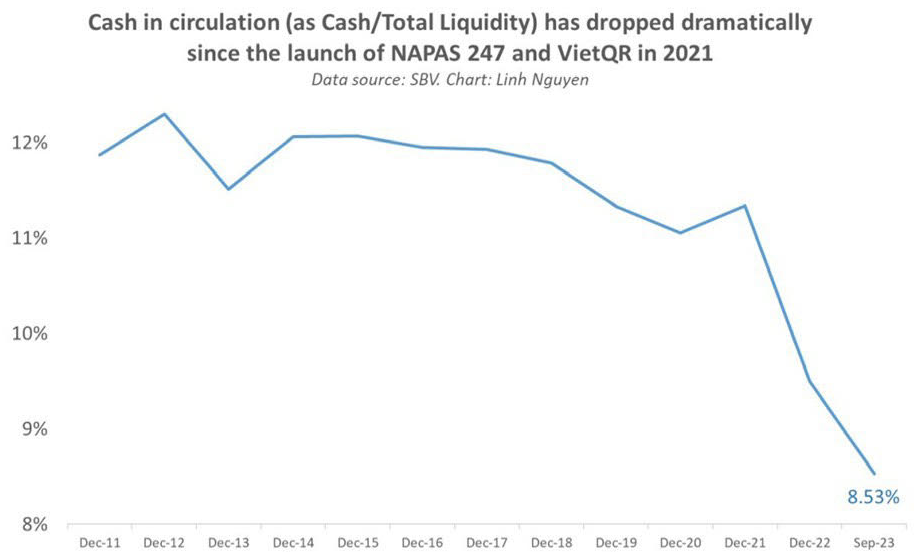

2 Here's a little-known impact: ↘ the sharp decline in cash circulation since 2021. It plummeted from over 11% to 8.5% by September 2023. To put it in perspective, it took a decade from 2011 to 2021 to reduce by roughly 1%. In contrast, the last two years saw a remarkable ~3% drop⏬. NAPAS had a clear mission statement: "to promote non-cash payment." Their journey was challenging but now the tide has turned. VietQR emerges as a pivotal player in this success story. 👑 🤔 What's VietQR? VietQR is a trademark for payment and money transfer using QR codes in Vietnam. VietQR belongs to NAPAS (National Payment Corporation of Vietnam). NAPAS is a unique entity, with 49% ownership vested in the State Bank of Vietnam (Vietnam’s central bank) and the remaining 51% distributed among 15 major commercial banks in Vietnam. Beyond Vietnam, VietQR works with a few foreign bank apps from Thailand and Cambodia. This lets Thai and Cambodian tourists use their bank apps to scan and pay in Vietnam using their own currencies. What are your thoughts on this digital revolution?

bf1d4f4d-f559-4f6f-a163-13bf4c839308|0|.0|27604f05-86ad-47ef-9e05-950bb762570c

Tags: Napas, 247

Stocks

by finandlife10/12/2023 21:29

"Nature does not hurry, yet everything is accomplished."

Lao Tzu

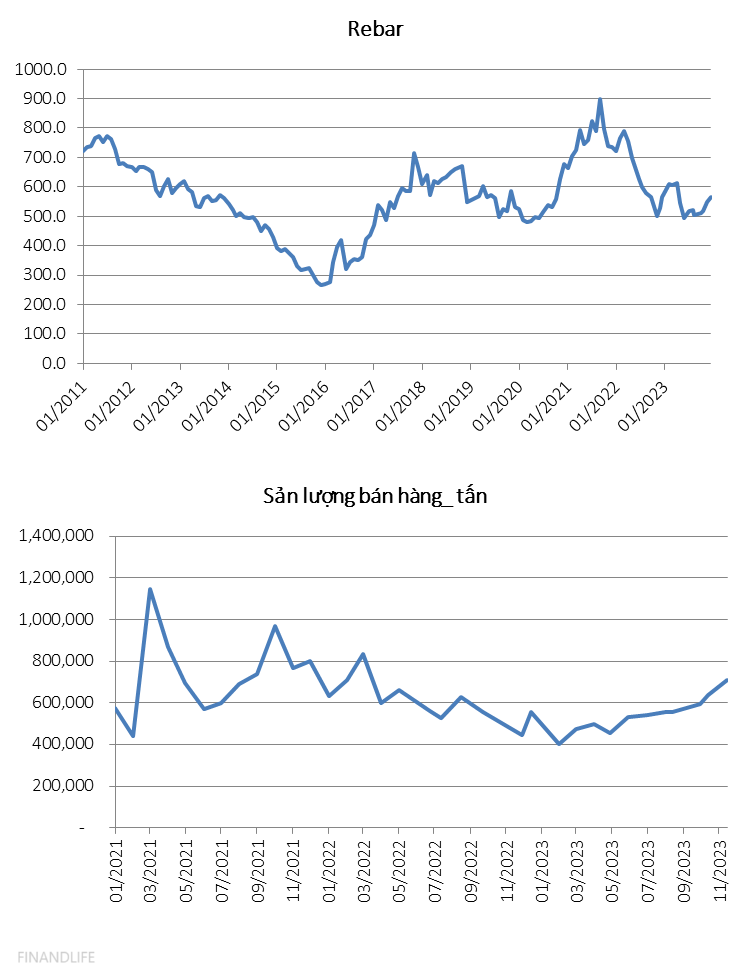

Giá thép tăng liên tiếp 3 tháng, sản lượng tiêu thụ liên tục tăng trưởng 11 tháng liên tiếp. Doanh thu 1 năm tới của HPG có thể đạt 140 ngàn tỷ đồng, lợi nhuận sau thuế có thể sớm tiếp cận mốc 18 ngàn tỷ.

Giá hợp lý mỗi cổ phần đang được các đầu phân tích lớn như VND, SSI, HCM ở quanh 33 ngàn đồng/cp, upside 18%.

FINANDLIFE

7c65b14b-bda3-41f7-a9b4-aa236b96a898|0|.0|27604f05-86ad-47ef-9e05-950bb762570c

Tags: HPG

Stocks

by finandlife19/11/2023 17:51“He who knows, does not speak. He who speaks, does not know.”

Lao Tzu

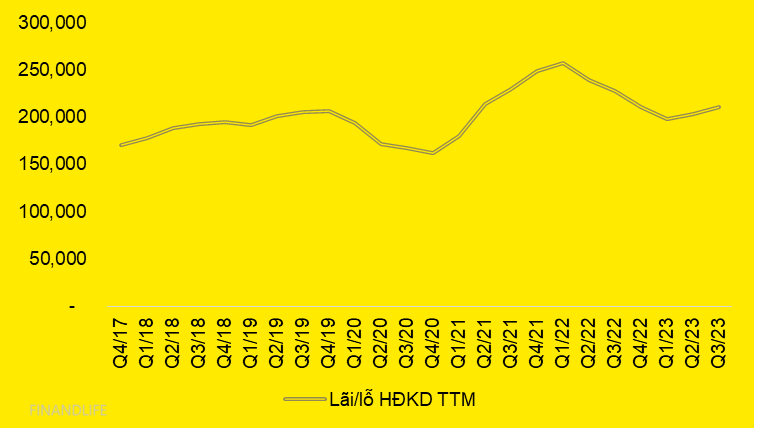

Kết quả kinh doanh quý 3 các doanh nghiệp niêm yết trên sàn chứng khoán Việt Nam (loại trừ các ngân hàng, tài chính, bất động sản) cho thấy sự cải thiện quý thứ 2 liên tiếp. Lợi nhuận hoạt động kinh doanh trượt 4 quý liên tiếp đạt 198 ngàn tỷ vào Q1/2023, tăng lên 204 ngàn tỷ vào Q2/2023, tiếp tục tăng lên 211 ngàn tỷ vào quý 3/2023. Biên lợi nhuận chính thức quay lại mức trung bình sau thời dài suy giảm do cách ly COVID-19, chiến tranh Nga-Ukraine, Vạn Thịnh Phát,…

English version as follows,

The business results of the third quarter of listed companies on the Vietnam stock exchange (excluding banks, financial institutions, and real estate) show improvement for the second consecutive quarter. Operating profits had improved for two consecutive quarters, reaching 198 trillion in Q1/2023, increasing to 204 trillion in Q2/2023, and continuing to rise to 211 trillion in Q3/2023. The official profit margin has returned to an average level after a period of decline due to the impact of COVID-19 isolation, the Russia-Ukraine war, Vạn Thịnh Phát, and other factors.

FINANDLIFE

efd84f58-dfd7-4af0-8102-73e240d0471d|1|5.0|27604f05-86ad-47ef-9e05-950bb762570c

Tags: KQKD

Economics | Stocks

by finandlife15/11/2023 16:57

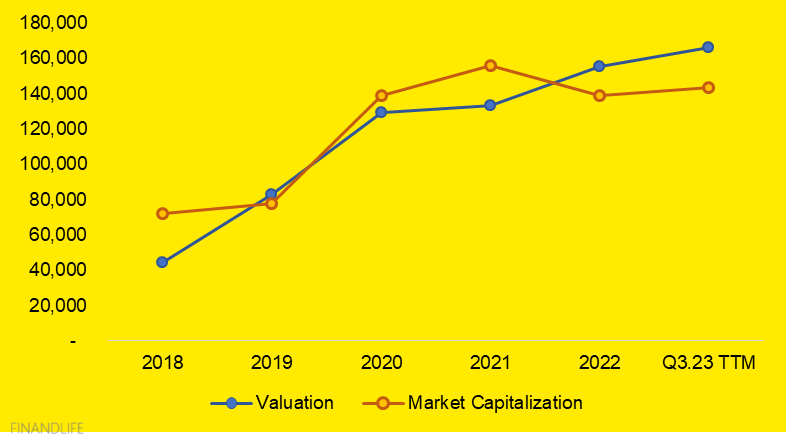

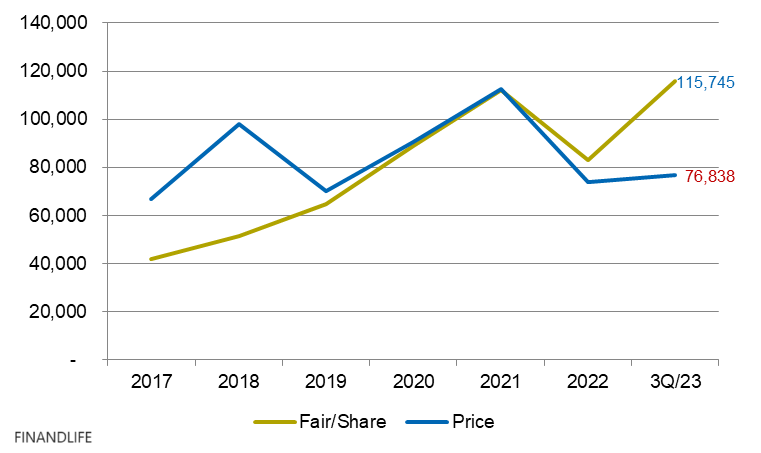

“Giá cổ phiếu sẽ vận động xoay quanh trục giá trị doanh nghiệp”

Công ty liên tục tăng trưởng, từ 12 ngàn tỷ doanh thu năm 2013, lên 17 ngàn tỷ năm 2018, lên 27 ngàn tỷ năm 2022. Kế hoạch 2023 đạt 31,500 tỷ đồng, +16.8%yoy.

Lợi nhuận sau thuế tăng từ 2 ngàn tỷ 2017 lên hơn 5 ngàn tỷ 2022. Kế hoạch năm 2023 đạt 6,500 tỷ, + 17.5% yoy.

Bảng cân đối kế toán ngày càng lành mạnh, nếu như nợ chiếm 46% tổng tài sản năm 2014 thì nay chỉ còn 36%. Công ty có tiền ròng 300 tỷ (Tổng tiền và tương đương lớn hơn nợ ngân hàng 300 tỷ đồng).

Mỗi năm công ty tạo ra 6 đến 7 ngàn tỷ dòng tiền. Đây là cổ máy tạo tiền quan trọng nhất của Tập Đoàn Masan.

Cổ tức tiền mặt chia trung bình 70-80% lợi nhuận làm ra. EPS trượt 4 quý đạt 9,155 đồng/cp, đã ứng tiền 4,500 đồng vào tháng 7/2023. Kỳ vọng cổ đông còn được nhận thêm >2000 đồng trong đại hội cổ đông sắp tới. Cổ tức tiền ròng mỗi năm quanh 6,800 đ/cp, tức suất sinh lãi cổ tức đạt 8.5%, rất hấp dẫn.

Giá trị hợp lý vốn hóa thị trường ước đạt 85 ngàn tỷ đồng, cao hơn 50% so với vốn hóa thị trường hiện tại.

Idea đầu tư: Mua một doanh nghiệp tiêu dùng hàng đầu với giá trị thật cao hơn 50% so với giá thị trường, chưa tính yếu tố tăng trưởng những năm tiếp theo. Được nhân cổ tức tiền mặt hàng năm >8%.

NOT BAD DEAL

1cf2b448-2614-4d18-a7ed-8814a0a8a051|1|5.0|27604f05-86ad-47ef-9e05-950bb762570c

Tags: MCH

Stocks